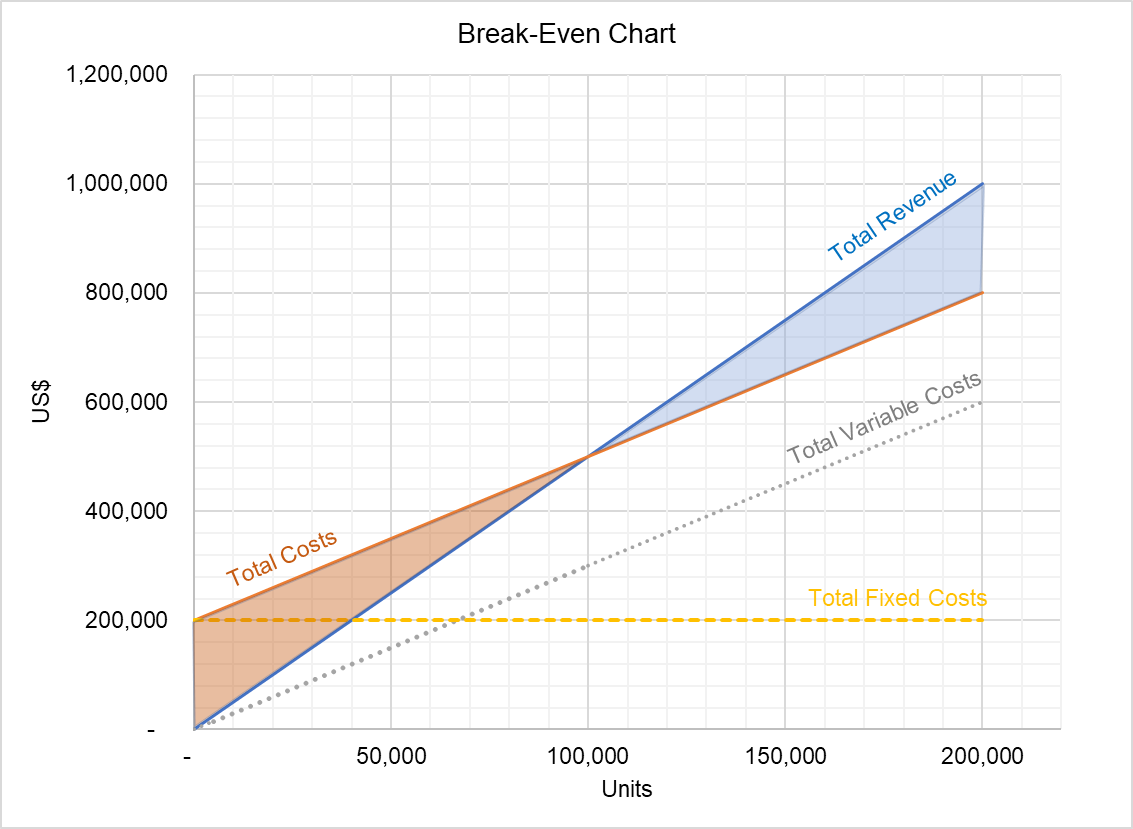

Conclusion Of Cvp Analysis : Cost Volume Profit Analysis And Decision Making In The Manufacturing : A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs).

Conclusion Of Cvp Analysis : Cost Volume Profit Analysis And Decision Making In The Manufacturing : A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs).. A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs). Cost volume profit analysis (cvp analysis), also commonly referred to as break even analysis, is a way for companies to determine how changes. Cvp analysis looks primarily at the effects of differing levels of activity on the financial results of a business. Cisco vvb integrated with cvp. If the manage is paid a commission of $6 blouse (in addition to the salesperson's commission).

Definition cvp analysis equation cvp analysis assumptions. How do changes affect profit? Cvp analysis also helpful when a business is trying to determine the level of sales to reach a targeted income. Cvp analysis looks primarily at the effects of differing levels of activity on the financial results of a business. Cost volume profit analysis shows how changes in product margins , prices, and unit volumes impact the profitability of a business.

Cvp Analysis Equation Graph And Example from xplaind.com A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs). Cvp evaluation highlights the connection between the associated fee, the gross sales worth, and the revenue. There are several different components that together make up cvp analysis. Cvp analysis looks primarily at the effects of differing levels of activity on the financial results of a business. The information in this document is based on these software and with the introduction of cisco vvb as a vxml browser, here is a sample trace analysis in order to track signals between cvp, ucce and vvb. The analysis is based on the classification of expenses as variable (expenses that vary in direct proportion to sales volume) or fixed (expenses that remain unchanged over the long term, irrespective of the sales volume). Managers use the contribution margin to plan for the business. Cost volume profit analysis shows how changes in product margins , prices, and unit volumes impact the profitability of a business.

At this breakeven point (bep), a company will experience no income or loss.

And those include, all costs can either be represented as fixed or variable. Certain underlying assumptions place definite limitations on the use of cvp analysis. Such assumptions include the following: It may provide very useful information particularly for a business that is commencing operations or facing difficult economic conditions. The information in this document is based on these software and with the introduction of cisco vvb as a vxml browser, here is a sample trace analysis in order to track signals between cvp, ucce and vvb. A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs). Cvp evaluation highlights the connection between the associated fee, the gross sales worth, and the revenue. Cvp analysis is only reliable if costs are fixed within a specified production level. The analysis is based on the classification of expenses as variable (expenses that vary in direct proportion to sales volume) or fixed (expenses that remain unchanged over the long term, irrespective of the sales volume). ••• b busco / getty images. When considering output decisions (e.g. Now that we have reviewed cvp analysis, you can probably note that it is an extremely simple and useful managerial tool. Managers use the contribution margin to plan for the business.

The contribution margin represents the amount. It may provide very useful information particularly for a business that is commencing operations or facing difficult economic conditions. The above analysis can be adapted to take into account multiple products rather than just one. The failure of cvp analysis to incorporate the cost of capital into a this paper proposes another variation of the cvp analytical model to include cost of capital on r&d investment and its risk level on strategic decisions. These components involve various calculations and ratios, which will be.

A Case Method Approach To Teaching Cost Volume Profit Analysis from demo.dokumen.tips Cvp analysis looks at the effect of sales volume variations on costs and operating profit. What would be net operating income or loss if company sells 18,500 blouses in a year? However, it has certain limitations because several simplifying assumptions are made in cvp analysis. Cvp analysis requires that all the company's costs, including manufacturing, selling, and administrative costs, be identified as variable or fixed. Such assumptions include the following: Cost volume profit analysis (cvp analysis), also commonly referred to as break even analysis, is a way for companies to determine how changes. It is sometimes referred to as contribution analysis because calculating break even requires determining how many service or product contributions (selling price per unit minus variable costs per unit) are necessary to cover, or. Key calculations when using cvp analysis are the contribution margin and the contribution margin ratio.

Cisco vvb integrated with cvp.

The information in this document is based on these software and with the introduction of cisco vvb as a vxml browser, here is a sample trace analysis in order to track signals between cvp, ucce and vvb. At this breakeven point (bep), a company will experience no income or loss. Cost volume profit analysis (cvp analysis), also commonly referred to as break even analysis, is a way for companies to determine how changes. The failure of cvp analysis to incorporate the cost of capital into a this paper proposes another variation of the cvp analytical model to include cost of capital on r&d investment and its risk level on strategic decisions. Cvp analysis looks primarily at the effects of differing levels of activity on the financial results of a business. However, it has certain limitations because several simplifying assumptions are made in cvp analysis. There are several different components that together make up cvp analysis. The above analysis can be adapted to take into account multiple products rather than just one. Cvp analysis is only reliable if costs are fixed within a specified production level. It is an analytical tool which is based on several cost accounting measures. The reliability of cvp lies in the assumptions it makes, including that the sales. The limitations simplify the process of analyzing the effect of changes in activity level to. It is sometimes referred to as contribution analysis because calculating break even requires determining how many service or product contributions (selling price per unit minus variable costs per unit) are necessary to cover, or.

How do changes affect profit? The reliability of cvp lies in the assumptions it makes, including that the sales. The failure of cvp analysis to incorporate the cost of capital into a this paper proposes another variation of the cvp analytical model to include cost of capital on r&d investment and its risk level on strategic decisions. It is sometimes referred to as contribution analysis because calculating break even requires determining how many service or product contributions (selling price per unit minus variable costs per unit) are necessary to cover, or. The above analysis can be adapted to take into account multiple products rather than just one.

Cvp Analysis Report Analysis And Features Total Assignment Help from www.totalassignmenthelp.com The limitations simplify the process of analyzing the effect of changes in activity level to. However, it has certain limitations because several simplifying assumptions are made in cvp analysis. These components involve various calculations and ratios, which will be. If the manage is paid a commission of $6 blouse (in addition to the salesperson's commission). Cisco vvb integrated with cvp. At this breakeven point (bep), a company will experience no income or loss. A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs). The analysis is based on the classification of expenses as variable (expenses that vary in direct proportion to sales volume) or fixed (expenses that remain unchanged over the long term, irrespective of the sales volume).

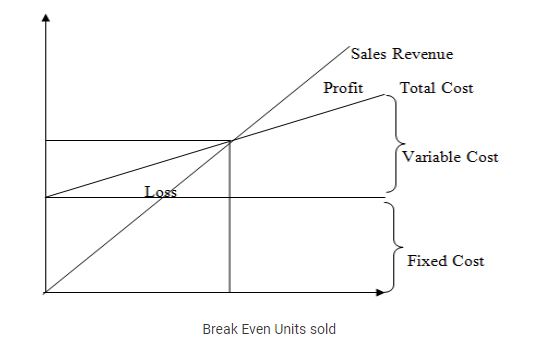

Cvp analysis looks at the effect of sales volume variations on costs and operating profit.

Key calculations when using cvp analysis are the contribution margin and the contribution margin ratio. Now that we have reviewed cvp analysis, you can probably note that it is an extremely simple and useful managerial tool. Every business organization works to maximize its profits. Selling prices and variable costs per. Cvp analysis also helpful when a business is trying to determine the level of sales to reach a targeted income. It is one of the fundamental financial analysis tools for ascertaining the breakeven point , given different cost levels and sales volumes. Managers use the contribution margin to plan for the business. The contribution margin represents the amount. Cvp analysis looks primarily at the effects of differing levels of activity on the financial results of a business. Certain underlying assumptions place definite limitations on the use of cvp analysis. The analysis is based on the classification of expenses as variable (expenses that vary in direct proportion to sales volume) or fixed (expenses that remain unchanged over the long term, irrespective of the sales volume). It may provide very useful information particularly for a business that is commencing operations or facing difficult economic conditions. Cost volume profit analysis (cvp analysis), also commonly referred to as break even analysis, is a way for companies to determine how changes.

A critical part of cvp analysis is the point where total revenues equal total costs (both fixed and variable costs) conclusion of cv. However, it has certain limitations because several simplifying assumptions are made in cvp analysis.

0 Komentar